WEST PALM BEACH, Fla. — My reporting this week on flood insurance in Florida has generated some emails from viewers, and especially some of you not happy with the premiums.

The flooding in many low risk flood areas earlier this month from Hurricane Debby did serve as a warning that flooding can occur nearly anywhere and all homeowners need to consider flood insurance.

However, the biggest response came when I reported that flood premiums in low risk areas can generally cost around $400.

“I just paid $929 for my flood insurance a few weeks ago,” read one email I received.

“$700 for this year and I am not in a flood zone,” read another.

I heard you loud and clear, and went to some experts about what’s going on.

“I would say if your flood insurance is $1,500 and you’re in Zone X, that’s telling something about the risk,” said Trevor Burgess, CEO of Neptune Flood Insurance in St. Petersburg, in reference to Federal Emergency Management Agency’s Zone X, which is considered a low risk area.

WATCH HERE: WPTV Matt Sczesny's previous coverage on how homeowners without flood insurance are impacted by Debby

He said his company has its own assessment of flooding risk and it’s not the same as the FEMA flood maps.

"Neptune ignores FEMA’s flood maps, because they’re out of date and not accurate," Burgess said.

Many insurance experts said the FEMA flood maps are only to determine if homeowners must buy flood insurance, and there are several factors that go into determining a premium.

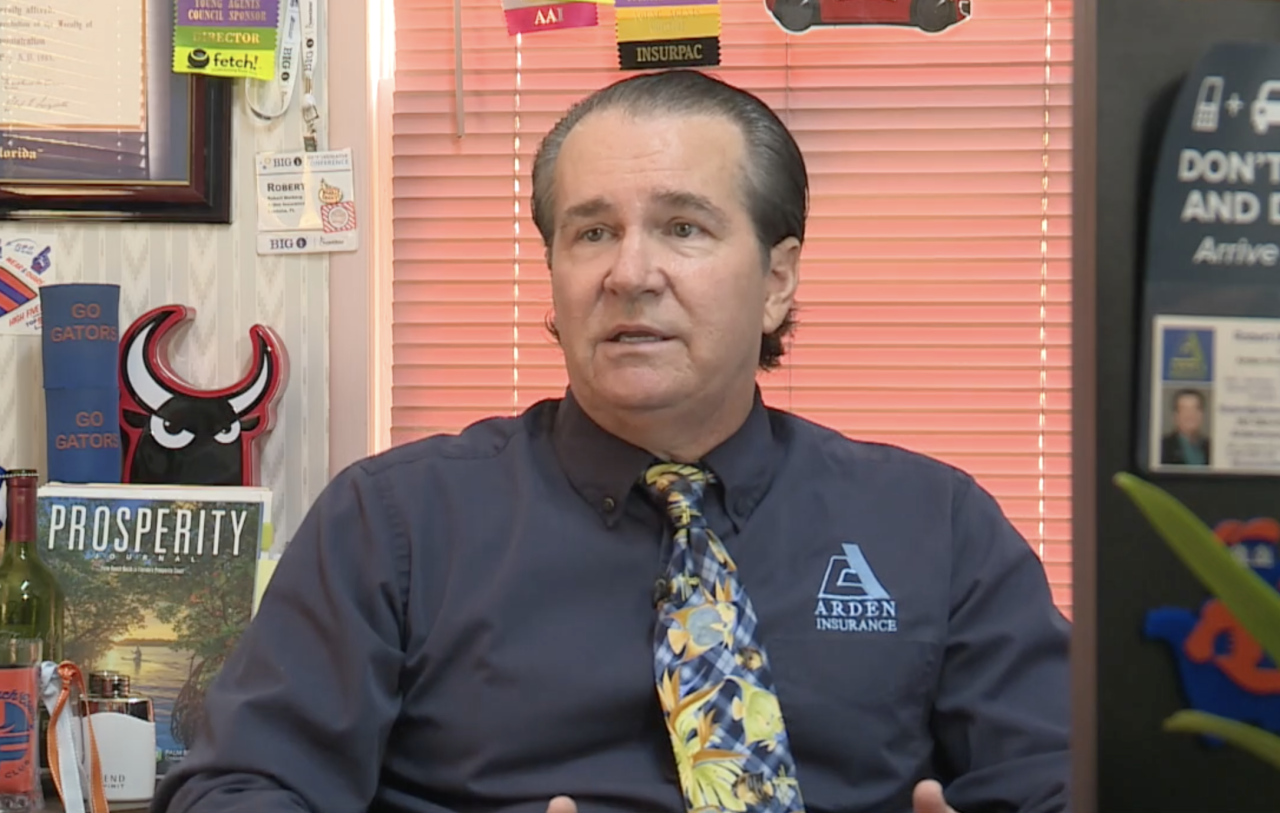

“You could be in a low hazard Zone X and still pay the same as your neighbor who’s in a high hazard Zone A,” said Robert Norberg of Arden Insurance in Lantana. “It’s based on the elevation in the area, the age of the house is now a factor, the replacement cost and rebuild cost is a factor, the way it’s built, whether its masonry or frame, is a factor.”

He also said homeowners in South Florida pay more for flood insurance than other parts of the state, because of the risk of powerful storms.

“Most of those people used to pay about $500 a year, it was the max in low hazard," Norberg said. "Now we’re seeing anywhere between $1,200 to $1,700 in low hazard.”

He said there is one solution, however. If you think you’re paying too much for flood insurance, get a flood elevation certificate.

“If you have a flood elevation certificate done by a surveyor, you can call them and give that to your agent," Norberg said. "They can send it in to your flood carrier and see if it does impact the rate.”

Matt Sczesny is determined every day to help you find solutions in Florida's coverage collapse. If you have a question or comment on homeowners insurance, you can reach out to him any time.

-

Fair quote or ripoff? How to get the best price on a big job

Need a bathroom or kitchen remodeled? Maybe a new driveway or deck? Some new digital tools will let you know if you are getting a good quote... or if you are about to overpay.

'Chipflation' sending laptop prices higher: How to beat the price hikes

Apple recently announced price hikes of $200 or more on its popular MacBook line, and other laptop makers are raising prices too. How to beat the price hike if you need a laptop this year.

Air travelers see higher prices despite lower oil costs

Airfares remain high despite falling fuel costs, helping major airlines post strong profits and push airline stocks higher.

Coupon stacking makes a comeback: How to pile up big savings at the register

Stacking coupons is not a thing of the past. While many coupons have gone digital, some stores still allow customers to combine multiple discounts in a single transaction — and the savings add up fast.