BOCA RATON, Fla. — Skyrocketing housing costs in Florida have local residents stressed about how they will pay their rent or find a place to live.

A new study released Tuesday by Florida Atlantic University is adding fuel to the frustration of many renters across the state.

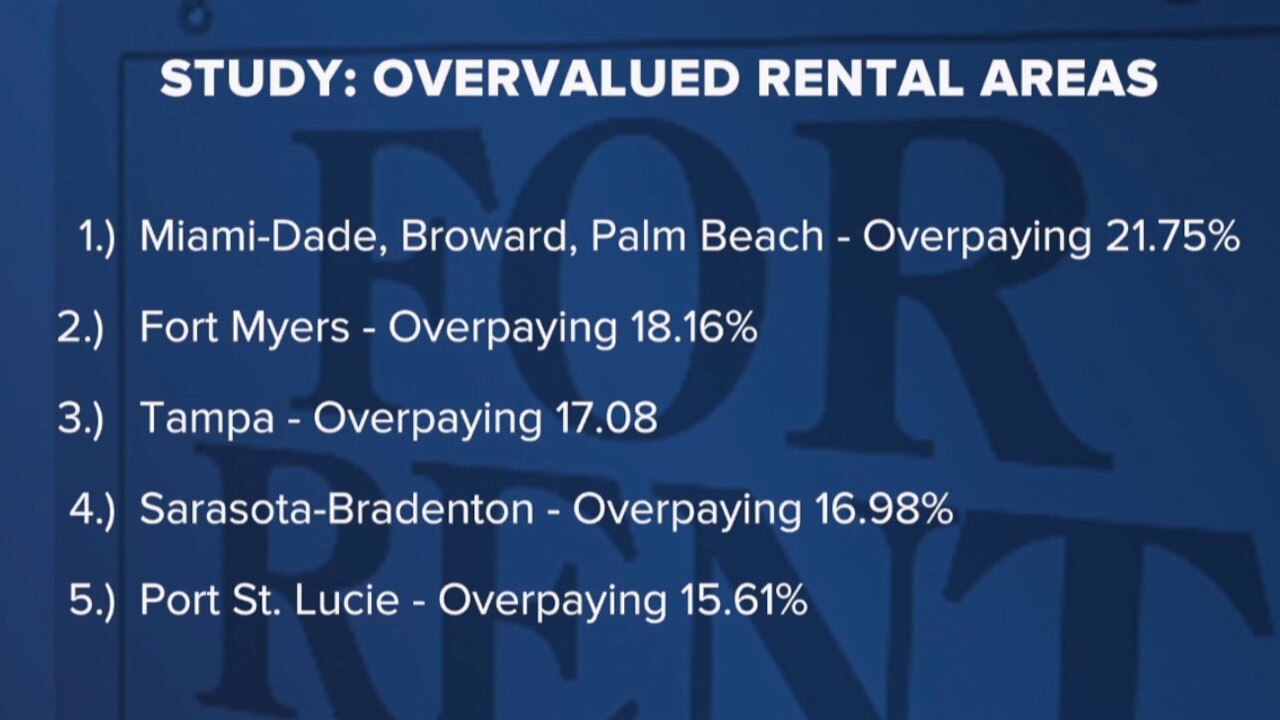

Researchers from FAU ranked the 25 most overvalued U.S. rental markets, and the first five were all in the Sunshine State.

The study found that renters in Miami-Dade, Broward and Palm Beach counties are paying an average of $2,832 a month — 21.75% above what they should be paying based on the area's long-term leasing trends.

RELATED: Renters face high costs, low inventory as housing crisis impacts South Florida

Other areas of Florida rounding out the top five of the study included:

- No. 2: Fort Myers has a $2,052 monthly average rent — 18.16% above the long-term leasing trend for the area

- No. 3: Tampa has a $2,029 monthly average rent — 17.08% premium above long-term leasing trends

- No. 4: Sarasota-Bradenton has a $2,402 monthly average rent— 16.98% premium above long-term leasing trends

- No. 5: Port St. Lucie has a $2,201 monthly average rent — 15.61% premium above long-term leasing trends

Other markets in Florida that made the top 25 of the list included Lakeland at No. 8, Daytona Beach at No. 12, Jacksonville at No. 13, Orlando at No. 16, and Melbourne at No. 19.

Researchers said they developed the list by analyzing rental markets in Florida earlier this year before expanding the study.

They used past leasing data from Zillow to model historic trends from 2014 to determine where rents should be and compared those to current rents.

Click here for a full list of the most overvalued U.S. rental markets.

Rent costs increased sharply in Florida during the pandemic due to robust demand from out-of-state transplants.

This came at a time when developers struggled to build more units because of supply-chain shortages and rising materials costs.

"Florida is a popular destination under normal circumstances, and it's even more desirable now because its pandemic policies strongly favored consumers and businesses," FAU real estate economist Ken Johnson said. "Landlords can charge exorbitant rents because if the existing tenants do not accept the new lease terms, other people will accept them quickly. This all points back to a persistent inventory shortage in rental units."

RELATED: South Florida home prices rising much faster than salaries

The study called the recent rent increases "unusual" because rents tend to be less volatile than housing prices, which are more reactionary to external forces, such as mortgage rate changes.

Johnson said they analyzed supply, demand, inventory size and inflation and discovered metro areas across the U.S. are overvalued, but South Florida is at the center.

"On average, we're paying 21 almost 22 percent of where we should be based on the history of prices," Johnson said. "Does that mean it's not worth it? Not necessarily because there's a huge scarcity with the supply of inventory of rental units right now and pretty much all over the U.S."

Johnson said when inflation eases we should see some prices drop, but he believes rental prices will not return where they were before the pandemic.

"Higher rents will persist until inflation comes under control and we build enough units," Florida Gulf Coast University real estate expert Shelton Weeks said. "In the meantime, people will have to make hard choices."

Researchers said a return to normal housing prices might not be happening anytime soon.

"We want an immediate solution to this problem, but there is none," said Bennie Waller, a professor of finance and real estate at

Longwood University. "There is going to be a reckoning from this latest housing crisis."